by Ivan Martchev

September 16, 2025

Another all-time high a fraction of a point above 6600 and another weak Friday close for the S&P 500. Last Friday it was only marginally negative, but we have had a string of three-negative Fridays, some of them big. It used to be that weak Fridays were a harbinger of bad news, but lately it has not been the case as investors are convinced that the Fed will cut by 25 or 50-basis points this Wednesday since job growth has been anemic and weekly jobless claims just spiked by 27,000 last Thursday to a four-year high.

The Fed has a dual mandate to fight inflation and promote job-growth. It looks like the job-growth part of the mandate is in need of more attention at the moment.

Weekly Jobless Claims

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

When I listed the long-term trend of weekly jobless claims last week, I suspected weaker jobless claims were coming soon as some metrics in the monthly payroll numbers (even before the recent downward revisions) were already suggesting a weakening of the job market for three months. To be fair we have spiked to the 250-260K range of weekly jobless claims in 2024 which turned out to be a 1- to 3-week wonder. But because the administration was focused on firing federal workers in February and March with six-month severance packages, it may turn out to be the case that those workers may show up in weekly jobless claims in September and October, if they have not found another job. Those federal workers plus any other that may have lost jobs in the normal order of business may end up pushing the weekly jobless claims past 300K, which I do not believe the stock market would like.

The stock market is happy as they are rooting for a 50 bps Fed rate cut but they may end up being satisfied even with a 25 bps cut if the Fed signals more rate cuts are coming. Typically, when the Fed cuts by 25 bps points it does not stop there, so we may be looking at three rate cuts this year. If there is no pickup in inflation in 2025, we may see more rate cuts next year. Since the Fed is cutting rates with the stock market at all-time highs, it stands to reason that it would be supportive but the stock market.

But one thing Fed rate cuts won’t do is deliver immediate jolt to the economy. My experience is that they work with a lag of 6-12 months. So, if the economy weakens further in 2025, no Fed rate cutting will help until 2026. That is not my base-case scenario but it sure is a possibility that needs to be considered.

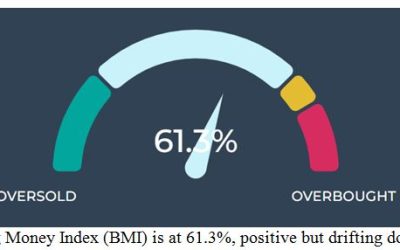

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

There are two possible reversal triggers this week that may mark a short-term top. One is the Fed meeting on Wednesday, and the other is the quad-witching options and September index futures expiration on Friday.

Why would the Fed FOMC meeting be a possible short-term reversal trigger?

Because everyone is sure the Fed will cut, and we have rallied 246 points (low to high) off the September low so far. A big rally into an expected event tends to produce a “sell the news” outcome in many cases. This is a very sharp rate of advance that is unsustainable, and we are due for a zag lower.

Still, unless we begin to trend below the 20-day moving average, it is nothing more than a pullback. Even if it is just a pullback when the market has gotten that extended to the upside since late July the pullbacks have been 2-5 days and between 140-215 S&P points (rounding the numbers). The maximum draw-down since late April has been a little over 3% while the rally–intra-day low to intra-day high–since April has been 36.5%. A 5-10% correction would be normal, but because many fund managers have under-performed in this rally, they are aggressively buying smaller dips.

The second possible reversal trigger is when both September futures and September monthly options expire on the same day, which is Friday. I have seen it several times how after a sizable rally this has turned out to be meaningful high for the market. No way to guarantee if this will be the case again but it is certainly something to keep in mind as between Wednesday and Friday the chances that we hit an intermediate-term high that sticks for a few weeks are better than even in my view.

I am only looking for normal seasonal correction, which is overdue in my opinion, and fresh all-time highs near 7,000 by year end.

The post 9-16-25: S&P 6600.21 appeared first on Navellier.