by Ivan Martchev

July 29, 2025

If you filter out any big moves (3% or larger) since we began to rally hard after the April bottom, you will see that there have not been very many corrections. In fact, there is a handy “zig-zag” indicator that measures those moves and it finds only one such better-than-3% zag, down 3.37% in mid-May.

Since mid-April, we have moved from 5,100 to 6,400 on the S&P 500 (rounding the numbers). That’s about 25% in a little over three-months, and we have seen only one meaningful correction.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Zig-zagging is normal, and going straight up or straight down is not, so this winning streak is something to keep in mind as we wrap up July. To be fair, the market has been overbought since before the July 4th holiday. But, as I wrote in May, “Overbought” Can Be a Nebulous Concept. It does not mean the market is going down. It may mean it goes sideways and continues to rally, which is what happened in our case.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

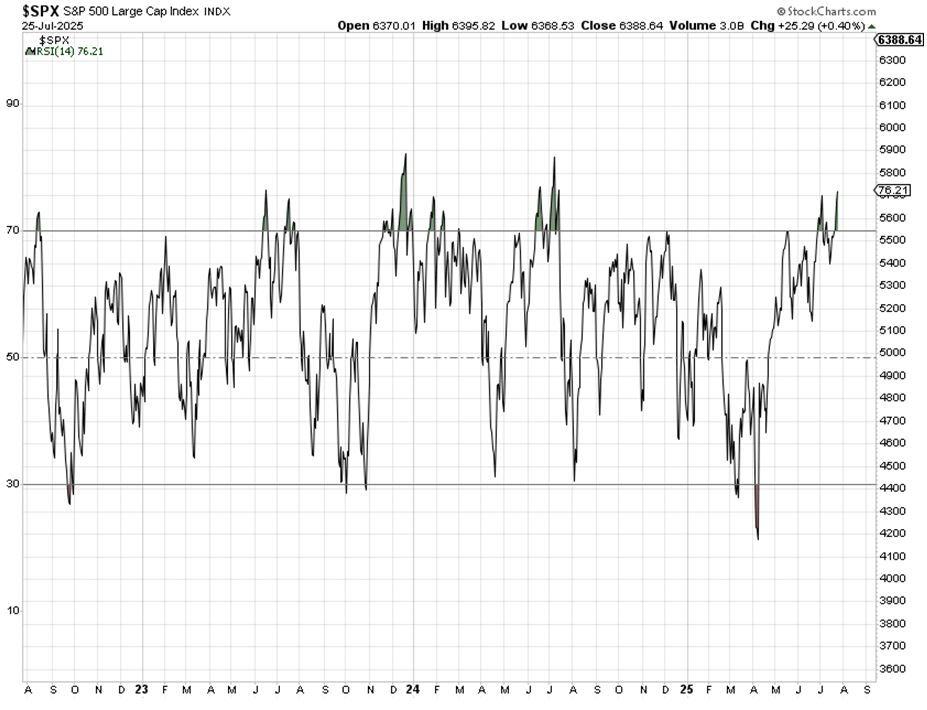

Still, the continued rally since May has resulted in the S&P 500 RSI oscillator reaching 76.21 on Friday, the highest reading of the year, so far. Typically, above 70 is considered high. This indicator rarely makes it to 75 for a major index like the S&P 500 and it has been above 80 only twice in three years – in December 2023 and July 2024. Further gains in the RSI oscillator at this point are unlikely. The more likely scenario is for the index to revert to the mean somewhat.

Earlier, I thought the lack of trade deals would trigger a correction, but so far that has not been the case. In fact, if trade deals, or more accurately, trade deal frameworks are announced with the EU and China, we may see some further gains, but the likelihood of a meaningful correction still remains high.

The reason why the market made it so far so fast without a correction is that many institutional investors assumed that the trade war would lead to a recession, but it hasn’t. Those concerned investors may remain underinvested, relative to their benchmarks. The S&P 500 has again advanced in a narrow fashion like it did in the first part of 2024, leaving portfolios not necessarily overweight in technology to underperform. Basically, we’re seeing institutional investors chasing the market because many are underperforming.

I still believe it is likely we will make it to 7,000 on the S&P 500 by year’s end, assuming the trade war threats wind down. If investors think more about lower taxes and deregulation, market advances will suddenly become easier to achieve. But I don’t believe this straight line advance higher with only one 3% draw-down in the last three months would continue for long.

I don’t know what will trigger a correction: It could be last minute trade issues, it could be something geopolitical. Last year saw a fierce rally in the yen that caught a lot of people by surprise, as there was a lot of borrowing in yen in order to buy U.S. stocks and bonds, an institutional type of carry trade that uses leverage where interest rates are the lowest, as is the case in Japan. The surging yen meant surging losses if institutions did not get rid of their yen-funded carry trades – and did so in a matter of two weeks.

This year I thought the trigger would be trade issues because of the lack of major trade deals, other than the one with Japan, but so far that has not been the case. Perhaps it is investors realizing that the tariff rates are so high that it would be cost-prohibitive not to strike some type of better deal. Because Canada is so dependent on U.S. trade it is very much doubtful those 35% tariff threats would stick for long. The Canadians are not operating from a position of power and sooner or later they will admit it to themselves.

One side effect of the big rally into the July earnings reporting period is that good earnings are met with less enthusiasm. Good reports do not produce big rebounds and bad reports produce big sell-offs, in many cases. Many stocks are up 30-50% from one report to the other and in many cases the rallies have already discounted the good results. It is still early in earnings season, but that has been my impression so far.

The post 7-29-25: The Longest Zig of 2025 appeared first on Navellier.