by Bryan Perry

July 22, 2025

Fully invested market participants are banking on several bullish levers to be pulled this week and next week, all leading up to the tariff deadline on Friday, August 1st. Among America’s largest trading partners, most have not yet hammered out any formal free trade agreements (FTAs) with the United States.

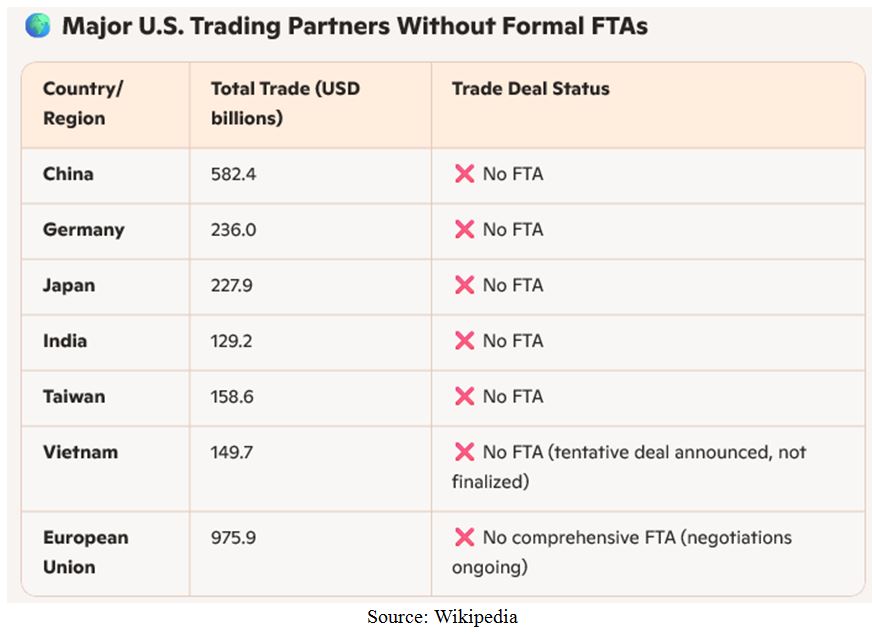

At the start of this week, the current status of America’s seven leading trade partners looks pretty dismal:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

From information now available, Vietnam and Indonesia have announced tentative accords with the U.S., but details remain unclear, and terms are not finalized, while our biggest trading partners have no FTA yet pending: The European Union (EU) is actively negotiating a framework agreement with the U.S. aiming to avoid 30% tariffs on all exports to the U.S. starting in August. India and Taiwan have expressed interest in deeper trade ties, but no formal agreements are in place, and Brazil is facing a crippling 50% tariff rate on imports to the U.S. unless they meet some specific political demands set by President Trump.

Japan and South Korea are facing 25% tariffs, with no definitive deals having been announced as of Sunday, July 20. China and the UK have seemingly cut deals or frameworks to avoid higher tariffs set for August 1st. So, with the clock ticking down to 10 days left to dicker, a large amount of progress needs to be made in a very short time, and whether the market cares about higher tariffs kicking in 10 days from now is highly uncertain. At present, a recent stock market rally shows little concern – it is more excited about how well the economy is performing, fueling optimism for the second-quarter reporting season.

Earnings will take the spotlight this week and next. With the market having rallied sharply in front of the heart of the reporting season, companies will have to beat estimates and raise guidance so as to maintain this bullish momentum. While there has been some tariff exposure that will impact second quarter results, the market wants to hear comments about any third quarter impacts if the August 1 deadline does, in fact, trigger steep reciprocal tariffs. Investors continue to believe the tariff risk will be broadly watered down.

We also face an eventful 10 days on the economic calendar (list, below). Investors will digest key reports involving existing and new home sales, durable goods, consumer confidence, the ADP employment data, the FOMC rate decision, the PCE inflation report and the employment data for July. All this information crosses the tape before the trade deal deadline. That’s a lot to digest, and surprises in any of these major indicators could trigger both bullish and bearish price pressure. Here’s a rundown of those indicators:

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

The Market’s Bullish Bias is Also Due to Renewed “AI” Buying

Clearly, a bullish market bias is in place, with much of the new money flowing into all things AI and the build-out of data centers domestically and globally. Global AI spending is projected to reach $360-billion in 2025, a 60% year-on-year increase. According to UBS, this spending momentum is expected to accelerate in 2026, reaching $480 billion, for another 33% increase. Even AI spending outside of the big four hyper-scalers (each of which is in The Magnificent 7) is expected to soar to $150 billion this year.

Currently, AWS, Azure and Google Cloud are the largest cloud providers in the world, generating tens of billions of dollars in revenue every quarter, growing at double-digit rates. A huge portion of this cloud revenue is reinvested into building and expanding their data centers and infrastructure that is dedicated to AI. The demand for AI services is rapidly growing, further fueling cloud revenues and creating a virtuous cycle, where AI drives cloud revenue, which in turn funds more AI investment. The general consensus is that the AI cycle is still in its early innings, which is solidly bullish for the stock market going forward.

So, while there will be some hand-wringing over the Fed and the looming tariff deadlines, in the grander scheme of things, the sensational spending cycle by every company to adopt an AI component to their business looks unstoppable for the next three to five years. Those who don’t employ AI in their business models will simply lose out in the long run. It is a must-spend category in order to compete in the future, and that is why most other market risks are being minimized, due to rising market and investor sentiment.

Yes, AI is that big.

The post 7-22-25: An Eventful 10-Days Await Both Bulls and Bears appeared first on Navellier.