by Bryan Perry

March 4, 2025

The noise level about the domestic economy downshifting from the strong finish in 2024 to that of a softer first quarter of 2025 is on the rise. There are several empirical and anecdotal points of evidence and fresh views from leading market economists that corroborate the facts (and growing narrative) that the Trump 2.0 trade has some wood left to chop to fortify some recently damaged investor sentiment.

Just to be clear, there are no hidden agenda items that are suddenly clouding the market’s landscape. The red wave that defined the November election remain – being tough on fentanyl, illegal human trafficking, sealing the borders, killing terrorists, punishing sanctuary cites, leveling the tariff playing field, getting out of Ukraine with a lasting peace and some well-deserved payback of military support, and rinsing the federal bureaucracy of needless workers, waste, fraud and abuse that helped build a $38 trillion deficit.

None of these policy goals should come as surprise out of left field. There are millions of people with non-essential jobs in the local, state, and federal government that are now feeling what it is like to live in the private sector. Corporations and businesses of all sizes constantly need to make hard decisions to survive and thrive. Congress and many government offices have offered near-lifetime job security, living very high on the hog for decades, and it is all coming home to roost. The debt-laden punch bowl is empty.

Multitudes of fraudsters within the orbit of government power, allocating public funds to businesses owned by families and friends, where some newly minted millionaires should not just lose their jobs, but do hard time, so the people that make up DOGE and the AI tools they are employing are doing a deep dive into the corruption. That does not sit very well in many parts of the DMV (DC, Maryland, Virginia) beltway bandit society that has lived extra-large on the sweat of everyday American taxpayers.

Markets have long ignored this oncoming train-wreck between the federal debt and the systemic government corruption controlled by Super Pac organizations that don’t care about fiscal responsibility – just power, control and short-term hyper wealth building. So, let’s look at what is influencing the bearish market sentiment and why the tough medicine being applied will result in a higher market by year end.

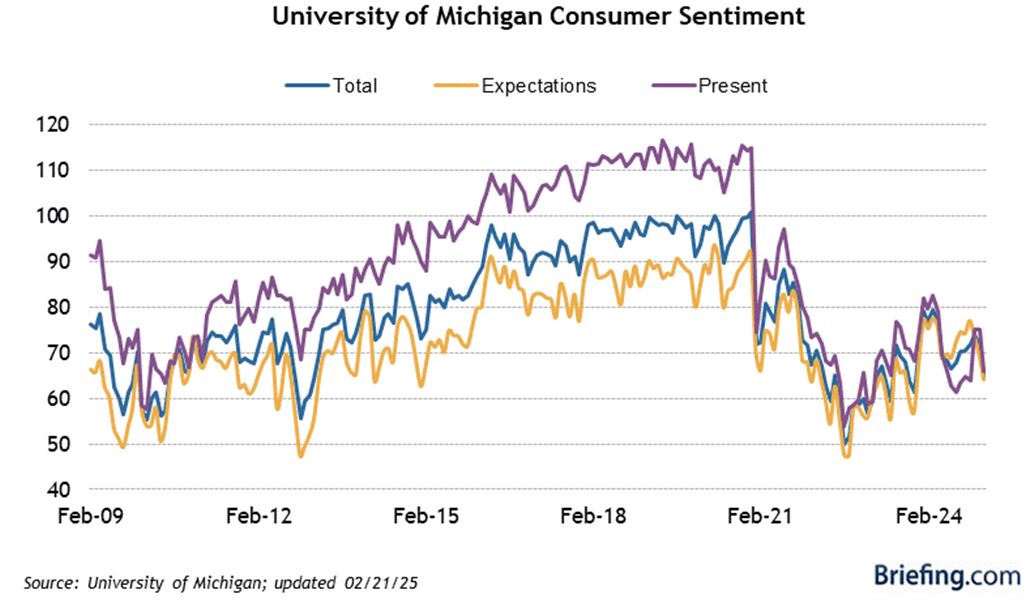

#1-The Cautious Consumer: The two most recent data points regarding the U.S. consumer came in well below forecast, the blame being laid on renewed concerns of inflation, the impact of tariffs and lower job security due in part to the federal layoffs. The final University of Michigan Index of Consumer Sentiment for February dropped to 64.7 (consensus 67.8) from the preliminary reading of 67.8, and the final reading for January was 71.7. In the same period a year ago, the index stood higher, at 76.9.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

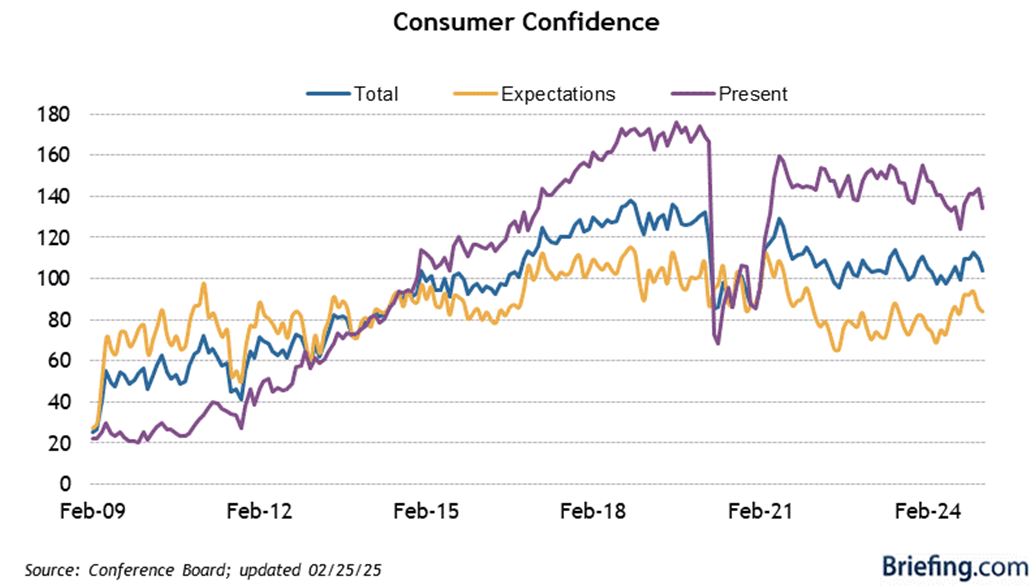

Also, the Conference Board’s Consumer Confidence Index dropped to 98.3 in February (consensus 103.1) from an upwardly revised 105.3 (from 104.1) in January, the largest monthly decline since August 2021.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

#2: The Weekly Initial Jobless Claims are Trending Higher: Initial jobless claims for the week ending February 22 increased by 22,000 to 242,000 (consensus: 220,000). Continuing jobless claims for the week ending February 15 were 1,867,000. The four-week moving average for initial claims increased by 8,500 to 224,000. The four-week moving average for continuing claims increased by 3,000 to 1,865,000. The key takeaway from this report is that initial jobless claims reached their highest level since early December, which will add to the market’s festering concerns about a growth slowdown.

#3: High-Profile Layoffs and Fewer Job Openings: I noted last week that the number and size of white-collar layoffs is rising. Chevron announced two weeks ago that they will lay off 20% of their global workforce, or roughly 8,000 employees. BP announced layoffs of 7,700. Microsoft announced an undisclosed number of layoffs. Meta announced another round of layoffs that comes to around 3,600 employees. Workday laid off about 1,750 employees, or 8.5% of staff, and Google is offering voluntary buyouts to workers in its platforms and devices units while Salesforce laid off 1,000 this month.

#4: Elimination of Non-Essential Government Jobs & Programs: Dante DeAntonio, labor economist for Moody’s Analytics, told FOX Business that the federal government has about three million workers, excluding the military, as of the start of 2025. He said that “the private sector should be able to absorb some of these workers. We estimate that about 100,000 federal workers have already been laid off or have accepted the deferred buyout offered by the Trump administration.” The biggest risk, he said, is that “the layoffs we have seen so far are just the tip of the iceberg. The magnitude and timing of future layoffs will determine whether the labor market can stay on the rails.” DeAntonio estimated that, “We currently expect that the size of the federal workforce will shrink by about 400,000 throughout 2025 due to a combination of the ongoing hiring freeze, deferred resignations, and DOGE-initiated layoffs.’

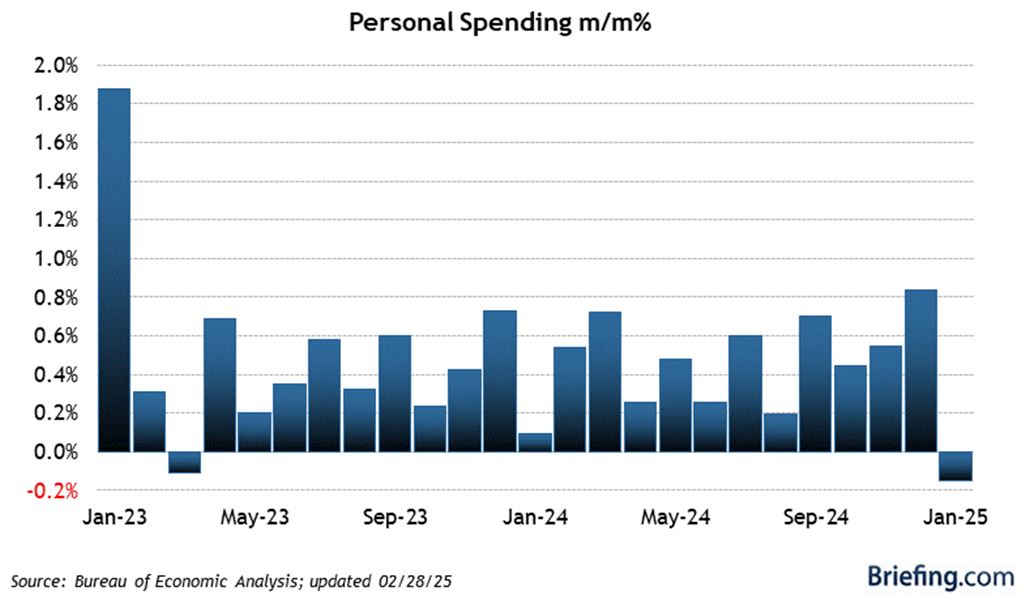

#5-The Personal Consumption Expenditures Index (PCE) Data is in “Goldilocks” Territory: The Fed’s preferred inflation measure, the PCE Price Index, was up 0.3% month-over-month, as expected, and up 2.5% year-over-year versus 2.6% in December. The core-PCE Price Index was up 0.3% and 2.6% year-over-year, moving nicely lower month-over month. At the same time, personal income increased by a robust 0.9% month-over-month in January (consensus 0.3%), led by a 1.8% jump in personal current transfer receipts, following a 0.4% increase in December, and personal spending declined 0.2% month-over-month (consensus 0.2%) following an upwardly revised 0.8% increase (from 0.7%) in December.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

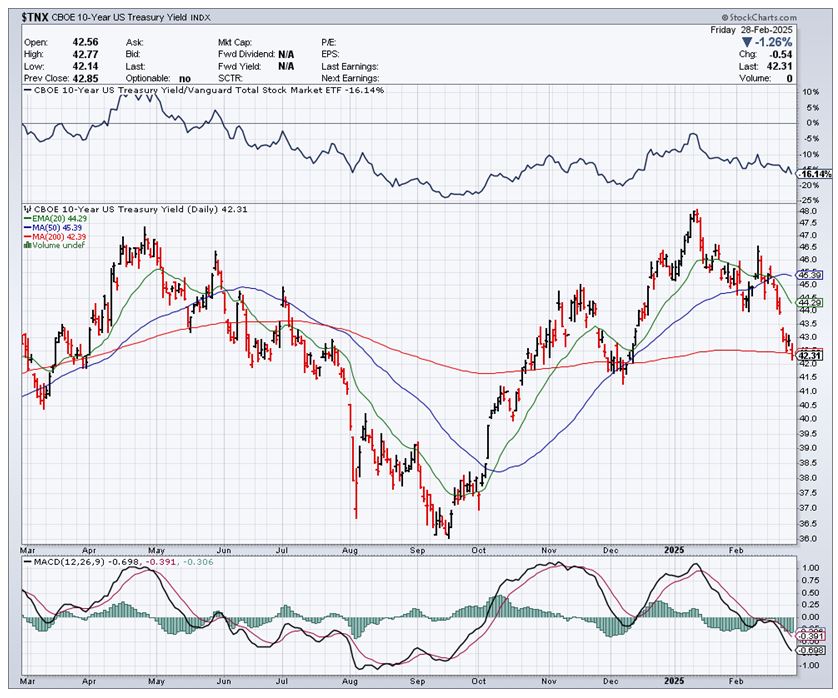

The above set of data points is just what the maligned bond market needed to right itself, and right itself it has, with the yield on the 10-year Treasury moving from 4.80% in mid-January to a current rate of 4.24%. This is a huge move, based on newfound fears of a recession grounded in uncertainty about the risk of trade wars, tariff-induced inflation, a widespread crackdown on illegal immigration, and the unknown future of all those non-essential government workers that now have to redefine themselves in other jobs.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

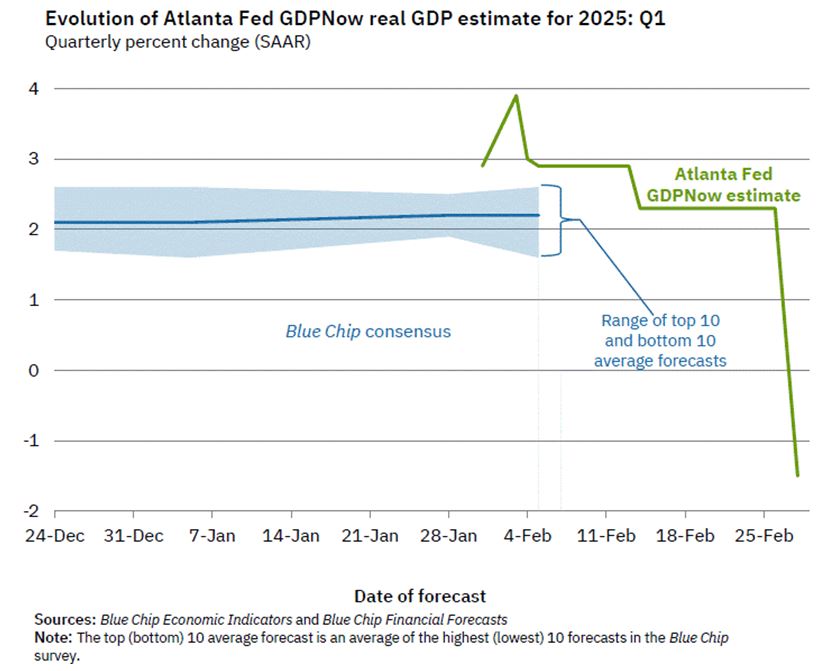

#6: The Latest GDPNow from the Atlanta Fed Has Turned Negative. The Atlanta Fed’s GDPNow model estimate for real GDP growth (at a seasonally adjusted annual rate) in the first quarter of 2025 is -1.5 percent, as of February 28, down from +2.3 percent on February 19. Really? A 3.8% swing in a single week over the threat of tariffs that may impact only 11% of the total U.S. economy.

This massive one drop is so drastic that I wonder if there is some political motivation here. The Atlanta Fed President, Raphael Bostic, was appointed in 2017 by the Senate in a campaign led by Senator Sherrod Brown (D-OH), ranking member of the U.S. Senate Committee on Banking, Housing and Urban Affairs, at the time citing the persistent lack of diversity among presidents and directors at the Fed’s 12 regional banks. One would hope a regional Fed isn’t shaping a statistical indicator due to its political agenda.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Regardless of whether the Atlanta GDPNow data is turning political, the job market is softening at a pace that is arguably picking up speed. Recall the Fed has a dual mandate: Keeping inflation low and striving for maximum employment. Currently, there is a 93% probably the Fed will keep the Fed funds rate unchanged at 4.25%-4.50% at the March 19 FOMC meeting, and a 30.2% probability the Fed lowers it by a quarter point at the May 7 FOMC meeting. I would contest that the Fed is once again behind the curve and will scramble by mid-year to counter an eroding job market that is just now showing some cracks.

Navellier & Associates own; Alphabet Inc. Class A (GOOGL), Microsoft Corp (MSFT), and Meta Platforms Inc. Class A (META), in some managed accounts. Navellier does not own; Chevron (CHV), or BP plc (BP). Bryan Perry does not own; Alphabet Inc. Class A (GOOGL), Microsoft Corp (MSFT), Meta Platforms Inc. Class A (META), Chevron (CHV), or BP plc (BP) personally.

The post 3-4-25: The Fed May Cut Rates Sooner Than Expected–to Deal with a Tighter Job Market appeared first on Navellier.