by Gary Alexander

November 12, 2024

Last Friday, after our regular weekly Market Mail conference call, I had the opportunity to join Louis Navellier and his daughter Crystal in a taping of Navellier Market Buzz. (Be sure to check out this new service each week on YouTube, and subscribe to it if you enjoy it).

In preparation for the interview, Crystal and Louis drafted five questions for me, and I tried to be brief in my “on air” answers, in order to give Louis plenty of airtime for his coverage of economic and stock-specific questions, which have more immediate impact to most of our subscribers. But in this column, I’ll list Crystal’s five questions to me and some more research, based on the data I referred to in my answers.

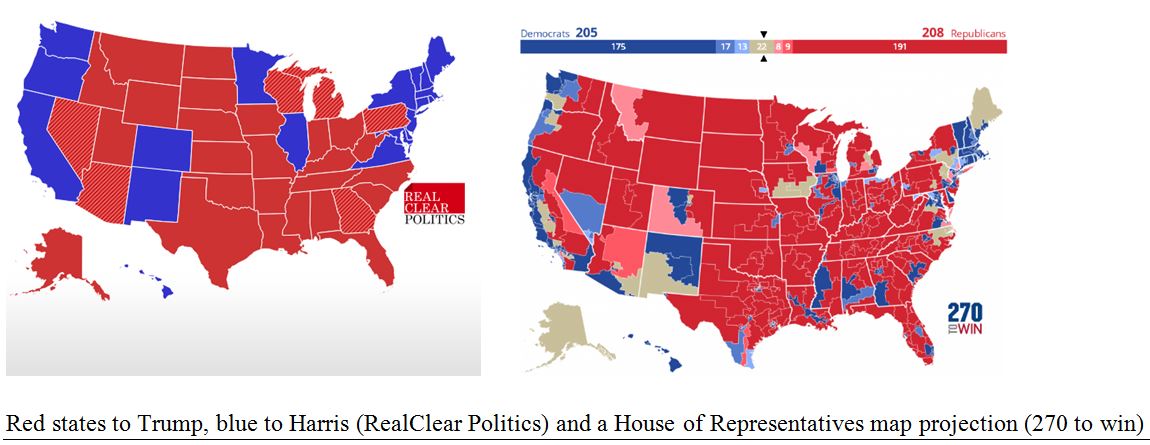

Question #1: Can you put into perspective what Tuesday’s election results mean for investors? Would you call this a political earthquake?

Yes, I would call this a political earthquake, since Trump not only won all seven “swing states” but Republicans also gained enough seats in both the Senate and (likely) the House to score the trifecta. The pollsters were mostly wrong, showing no gap in swing states and popular votes in Harris’s favor, when the popular vote was +3-4 million for Trump. Although media bias tilted blue, they did not influence many.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Another “earthquake” measure is that Trump gained a greater percentage of votes in all 50 states. Trump also gained in percentage of votes among black, Asian, Hispanic and youth, in some cases doubling his 2020 totals. The market likes certainty, and this election was “certainly certain.” Trump was declared the winner at 10:45 pm Tuesday (Pacific time), so I expected the markets would celebrate the next day.

Sure enough, the Dow gained over 1,500 points on Wednesday, its best single day since the COVID days of March and April of 2000. NASDAQ gained 544 points (+3%) and the more domestic-focused small-stock Russell 2000 did best, up 5.84% on Wednesday and setting a three-year high then, and on Friday.

Question #2: It appears that this was a low turnout election, since Donald Trump got almost the same number of votes that he did in 2020, but Kamala Harris only got 68.2 million votes, while Joe Biden got over 82.2 million back in 2020 … so how did 14 million Democratic votes disappear?

This is a premature assumption, so far, since (as of Sunday) California still has about 3.5 million votes left to count, and that is a heavily Democratic state. A few other blue states have a few hundred thousand votes uncounted, so Harris could reach 72 to 75 million votes – still 7-10 million short of Biden in 2020.

Harris earning far fewer votes than Biden underlines her weakness as a late appointment to replace Biden, but the Democrats didn’t use the full court press they staged in 2000, when the margin was “enhanced” (not stolen) by a well-funded campaign of vote harvesting among groups who seldom voted in the past. Consider this: Donald Trump gained 11.2 million more votes in 2020 than in 2016. Before 2020, no Republican candidate had ever received over 63 million votes, but he got 74 million in 2020 and lost.

That seemed a bit odd, at the time. Over the last century, every other incumbent that ran for re-election with such a huge gain in votes won in a landslide. The only incumbents running for re-election who lost had a huge (15% to 20%) loss in vote totals, for obvious reasons: (1) Herbert Hoover’s 1932 depression, (2) Jimmy Carter’s 1980 malaise and (3) George Bush, Sr., due mostly to Perot’s 20% vote grab in 1992.

So, how did incumbent Trump lose in 2020 with 11.2 million more votes than he earned in 2016? The obvious answer is funding by Mark Zuckerberg (“Zuckerbucks”) in key swing states, and poll harvesters passing out ballots to youth, retirement homes, inner cities and other concentrations of low-voting groups.

Since America has such low voter turnout (normally 50% of those over 18), it would be fairly easy to register and push voting on millions of those who normally don’t vote, if you have the manpower, desire and dollars, which Democrats clearly had in 2020 – powers they did not muster in 2024. Trump should have conceded 2020, in my view. The election wasn’t stolen, but perhaps it was “rigged” by this all-out blue blitz. Historians can debate this, but Mollie Hemingway’s book “Rigged” is a good starting point.

One final point: California’s slow vote count over the last week has held up decision time on eight House seats, putting House control in limbo, but the Republicans need only two more seats to gain a majority and four California districts and two in Alaska and Arizona (8 of 10 undecided seats) lean Republican.

Florida and Texas, the 2nd and 3rd most populous states after California, counted 99% of their votes last Tuesday night, but California allows itself the lazy luxury of a full week to deliver its vote count, since mailed ballots with a Tuesday, November 5th (or earlier) postmark are allowed a week to snail their way to a tabulation desk. This is simply poor management. My little island has a drop box at the fire station. There is no reason ballots need to remain in limbo for a week, if we can drop them in a local polling box.

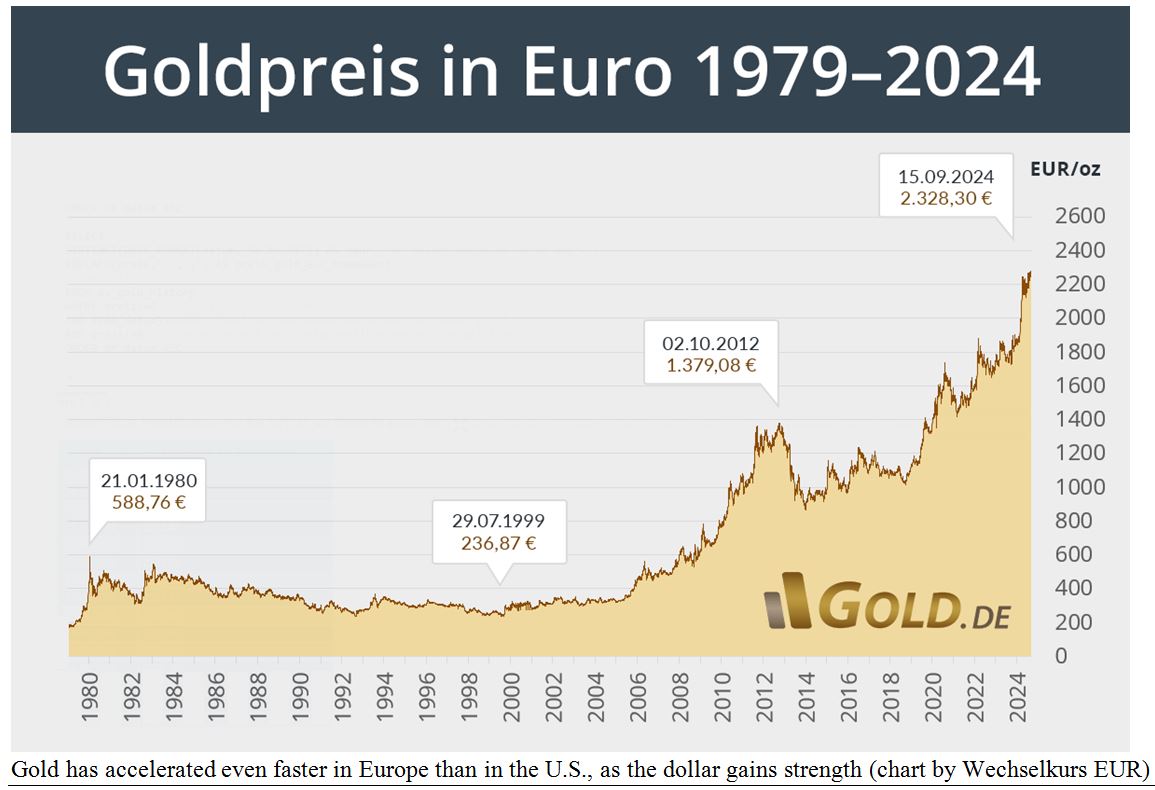

Question #3: The U.S. dollar surged after the election and Treasury bond yields rose, but gold fell. Is that because investors have confidence in the U.S. economy? Do you expect gold prices to recover?

There were some immediate overreactions by traders with itchy online trading fingers, so we saw huge moves in many markets on Wednesday. While stocks generally held on to their gains, the initial surge in the 10-year Treasury rate, and the fall in gold, were reversed the next day, while the U.S. dollar held firm. To answer your first question, yes, that shows greater confidence in the United States after this election.

Last Wednesday, the 10-year Treasury rate shot up from 4.30% to 4.47% on day after the election, but it reverted back to 4.30% by Friday. Some of the fear of higher rates comes from President-elect Trump’s tariff rhetoric, but I expect that he will treat tariffs more like bargaining chips and threats in negotiations, mostly to reduce other nations’ super high tariffs (compared to ours), not as permanently high tariffs.

Gold has recovered, and I expect it will keep climbing, though more slowly, in 2025, unless all global tensions immediately end, the budget is suddenly balanced, and inflation is flat. Gold is historically an insurance policy, not only an inflation hedge but a crisis hedge, and currency hedge. Last week, gold futures closed Tuesday at $2,740 and dipped under $2,660 the next day, but recovered to $2,688 on Friday, for a net decline of 1.9%, not bad, considering the landslide “earthquake” you mentioned.

Gold has been setting new highs in U.S. dollar terms this year, even as inflation has receded and the dollar has strengthened, which means that gold is setting even higher highs in terms of many other currencies.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

As for the U.S. dollar, it should keep rising if the Fed stops cutting rates and the world pours more money into the dollar. However, central banks have loaded up on gold even faster than dollars. especially in the last three years, with over 1,000 metric tons per year (a metric ton is one million grams, or 32,150 Troy ounces, so 1,000 tons of gold is currently worth about $85 billion added to central bank holdings each year), supplanting the euro as the #2 holding (behind dollars) in central bank coffers. There will be no return to an official gold standard, but central banks prefer gold over paper.

Question #4: Assuming the Republicans gain control of both houses of Congress, how does the stock market perform when one party has control of both houses of Congress and the White House?

I have long championed the compromise of government “gridlock,” in which one party controls the White House and the other runs Congress, creating checks and balances against governmental overreach by either party. Historically, since 1950, the S&P 500 averages 14.5% gains per year in gridlock years.

A great example of positive effect of gridlock is the side-by-side comparison of Clinton in 1993-94, when Democrats had control: Hillary was trying to nationalize health care and the S&P 500 gained only 5.6% in those two years, but after the Republicans took over Congress in 1994, the S&P 500 enjoyed five straight years of mega-gains: +34.1%, +20.3%, +31.0%, +26.7% and +19.5% for a 5-year 220% gain (1995-99), and four balanced budgets at the end of the century, 1998-2001. (The birth of the Internet also helped).

When it comes to one-party monopolies, the Democrats have swept the House, Senate and White House in nine elections since 1950, with a tepid average S&P 500 gain of 6.7% per year, while four Republican sweeps (a smaller sample) have averaged +13.5%, double the all-Democrat sweeps, and nearly as good as gridlock. Here is a quick summary of those eight years (four elections) when Republican ruled the roost:

- 1953-54: Dwight Eisenhower’s first two years generated +35.4% in S&P 500 and +38.5% in the Dow.

- 2003-06: George W. Bush’s middle four years delivered +61.2% in S&P 500 and +49.4% in the Dow.

- 2017-18: Donald Trump’s first two years were more muted: +12% in the S&P 500 and +18% in the Dow.

This doesn’t guarantee any gains going forward, but the odds are better than in a Democratic sweep.

Question #5: Where is Lopez Island, where you live? I assume your electricity in Washington State is mostly hydroelectric. There are AI data centers that Oregon and Washington have on the Columbia River due to all the hydro-electric plants, so do you think it is possible that Trump can double the electric grid to power the AI expansion anticipated in the upcoming years?

Lopez Island is the first ferry stop in the San Juan Island chain. Our “Friendly Island” (like a small town, we mostly know one another, so every driver waves at every other driver) voted 75%+ for Kamala Harris, a greater share than any other Washington county, including the biggest county, King County (Seattle).

We are close to Canada (Victoria BC is 25 miles west). We are Americans because of the outcome of the Pig War (1859-72), when a Yankee squatter shot a British pig and made Canadian bacon, causing armies from both nations to set up camps here, preparing for a war that never happened. Finally, an arbitration panel headed by German Kaiser Wilhem awarded most of the islands to America. Thank you, Germany.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

To your point, 85% of our electric power is administered by our local collective and connected to the mainland by underwater cable, eventually coming from hydro-electric power generated by the multi-dam Columbia River system. We will have huge energy demands in the future, partly due to AI expansion, and I fear our river system won’t be able to meet those needs, as there is a Western drought which has reduced Columbia River volume lately. We will need new sources. In last week’s Statewide election, Washington voters narrowly overturned a natural gas ban by 51% to 49%, so that is a hopeful start. With Trump’s expansive energy development policies, he’ll likely tap other sources to help supply meet rising demands.

The post 11-12-24: The Market Implications of a Republican Sweep appeared first on Navellier.